The Economy

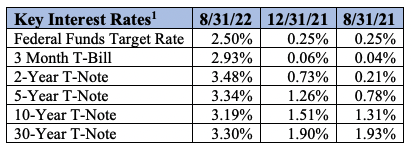

Another month of up and down reports on our burgeoning economy, capped off by Federal Reserve (the “Fed”) Chairman Jerome Powell’s hawkish remarks in Jackson Hole, Wyoming in his annual policy speech on Friday, August 26th. Powell stated that the Fed will “use our tools forcefully” to control the inflation that is still running near its highest level in more than 40 years, and that higher interest rates should be here “for some time”. After these comments, the markets are now predicting that the Fed Funds rate will increase to as high as 3.5-4.0% from the current level of 2.50%. Of course, the primary concern is how much these higher rates will curtail economic growth and employment, in other words, whether they can engineer a “soft landing” – lower inflation while not creating a recession – something that has proven difficult in the past. Speaking of recession, most economists are expecting one by early next year, but also claiming that due to low unemployment and relatively solid demand that we aren’t in one yet regardless of the two consecutive quarterly declines in Gross Domestic Product (GDP – the primary measurement of all goods and services produced in the U.S.). On that note, second quarter GDP was revised upward in August from the primary reading of negative -0.9% to a much better negative -0.6% according to the Bureau of Economic Analysis. The only other primary economic indicators that are coming in below expectations are those associated with housing, not entirely unexpected with higher mortgage rates, inflation, and supply chain issues. Excluding interest rates and housing, most other indicators are healthy. Unemployment is at a healthy low rate of 3.7%. Inflation, after months of increases, came in flat month-over-month in July, still not declining but the annual rate is now 8.5% vs. June’s 9.1%. Consumer confidence is increasing, and most of the manufacturing reports still indicate an expanding economy. Regardless, it will be a struggle to maintain a growing economy with rising interest rates.2

The Markets

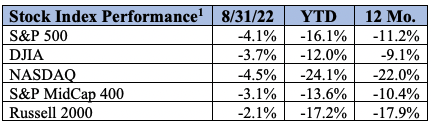

The month of July, the best for the markets since November 2020, was of course followed by the difficulties in August primed by the forecasted hawkishness in the Fed. The S&P 500 Index was down 4.1% on the month, 17.6% below its all-time closing high of 4,796.56 set on January 3, 2022, and down 16.25% year-to-date. The S&P MidCap 400 and the small cap Russell 2000 also posted negative total returns, coming in at -3.1% and -2.1%, respectively, although better than their large cap brethren. The NASDAQ Composite lost 4.5%, as the growth companies that represent a large portion of this index are especially vulnerable to higher interest rates. All four of these indices are in bear market territory, which is defined as a price drop of 20% or more from the most recent peak price of a security or index. The only one of the major indices that is not in bear market territory is the Dow Jones Industrial Average (DJIA), and the DJIA posted a loss of 3.7%. Only 2 of the 11 major sectors that comprise the S&P 500 index posted gains in August, with Energy up 2.8% and Utilities up 0.5%. Energy also leads year-to-date, up 48.5%. Information Technology was the laggard, dropping 6.1% for the month, with Communications exhibiting the poorest performance in the last 12 months, down 35.2%.3

Outlook

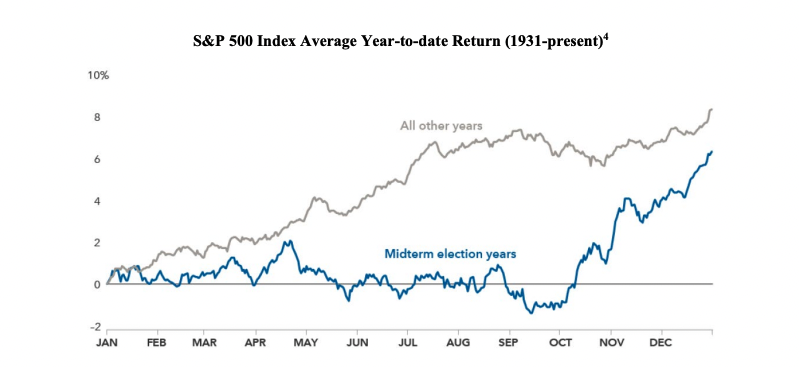

Volatility: this is what we have seen for some time, and especially evident after July’s solid gains followed by August’s turbulence. An important thing to remember is that volatility is normal, will always be with us, and should not affect your investment strategy. Of note is that mid-term election years tend to exhibit greater volatility than normal, with poor or flat market returns prior to the election and solidly positive results after the polls have closed (see chart above). Markets do not like uncertainty, hence the greater volatility prior to November, and, as the chart shows, the markets tend to rally after the mid-terms. In fact, the annualized return using November 5th as a proxy for post-midterm results is 15.1% vs. 6.8% for all other years. Remember that every year is different, but the prudent investor will remember that short-term volatility is part of long-term returns.5 As always, there are many risks to the short-term returns in the markets. Higher interest rates will slow the economy further and make earnings comparisons more difficult. Geopolitical risks abound. We are still in a bear market, but this means that opportunities abound to invest at discounted prices. We are committed to US capital markets and think the long term will be rewarding. Most of all, stay the course and stick to your investment plan.

- 1 Sources: Bloomberg and Investment Company Institute; total returns

- 2 Source: First Trust Portfolios L.P, CNBC.com

- 3 Source: Standard & Poor’s

- 4,5 Sources: Capital Group, RIMES, Standard & Poors. As of 8/31/18, Results in USD

DISCLOSURE: Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.