Will Rising Fuel Prices and the Invasion of Ukraine Crush the Bull Market?

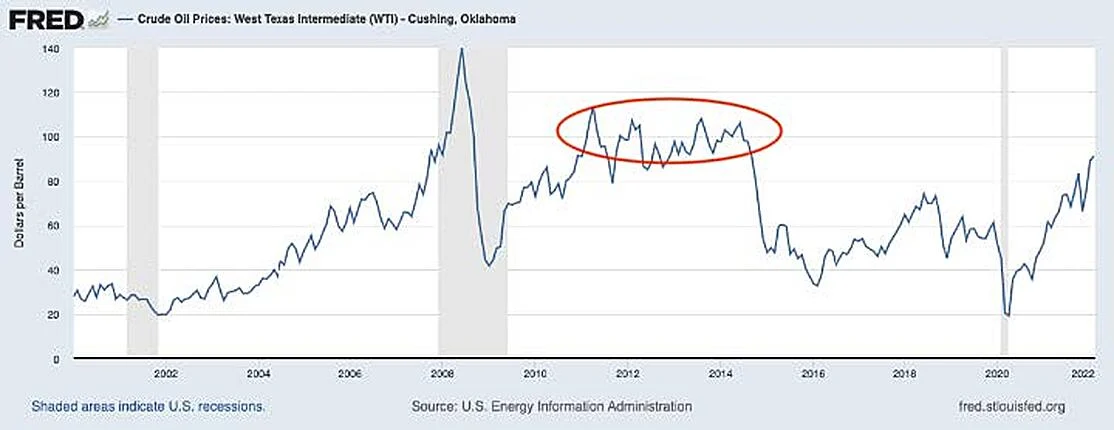

Oil prices have been marching higher for months, a fact that many likely know based on recent trips to the pump. The cost of a barrel of West Texas Intermediate oil has soared from the low teens in April 2020 to over $90 a barrel today, as surging demand continues to be met with constrained supply. Many economic forecasters and energy analysts are calling for $100 per barrel and soon.1

If oil prices continue to move higher, costs for businesses and consumers will continue to go up as well, which could sap margins and spending, respectively. This begs the question: will high oil and gas prices crush this bull market?

We think the answer is no. The first reason we’ll give is based purely on history, and the second reason is based on a supply and demand imbalance we think should correct later this year.

Let’s start with the history. Many may not remember, but there was a period from mid-2011 to 2014 when oil prices hovered around $100 a barrel pretty consistently (circled in red on the chart below). Gas prices were quite high then, too, even higher than they are in parts of the country today.

The stock market did not seem to mind – during the period from 2011 to 2014 when a barrel of oil cost more than $100, the S&P 500 went up +65.1%.2 The U.S. economy grew throughout that period as well, albeit at modest rates. Modest GDP growth was more due to the economic ‘hangover’ from the Global Financial Crisis than high oil prices, in our view.

The first chart below shows the period when oil was above $100 a barrel, and the second chart shows the S&P 500 from 2012 onward. As you can see, higher oil prices may not have necessarily helped the economy and markets, but they certainly did not hurt.

The second reason we do not think higher oil prices will kill the economic expansion and/or bull market is because of supply forces.

The period of high oil prices from 2011 to 2014 gave way to a shale boom in the U.S., which, coupled with OPEC also increasing supply, caused oil prices to plummet (you can see the drop-off in prices around 2015). The well-remembered U.S. shale boom was heavily financed with debt, which ultimately led to a wave of bankruptcies and failed companies when oil prices crashed. Some analysts believe the lessons learned in that period will result in broad reluctance for shale producers to take advantage of high oil prices this time around, meaning supply will remain constrained in 2022. But the data so far suggests otherwise.

In the U.S. Permian basin, shale exploration and development rig activity are back to about 70% of pre-pandemic levels, and oil production is close to crossing all-time highs above 5 million barrels per day. In the gas-rich Haynesville close to the U.S. Gulf Coast, activity is just about at its highest level in a decade. U.S. oil production in February is expected to rise to 8.54 million barrels per day, which is only 730,000 barrels less than the record set in November 2019. Back then, oil prices were $20 lower than they are today.

At the end of the day, U.S. shale producers are very wary of taking on big debt and overproducing as they have in the past. But they are not wary of ramping up production to take advantage of higher prices. As of late last year, the break-even cost for shale producers was $37 per barrel. With oil trading above $90 per barrel, the incentive to come back online is high.

The other side of the supply equation is, of course, OPEC. The organization has indicated on a few occasions its intention to increase production and most recently announced a 400,000 barrel-per-day increase in March. But figures from OPEC are not always reliable, and to date, OPEC production remains about 5 million barrels per day below peak levels. Market-watchers are understandably worried about the impact of the Russian invasion of Ukraine, given Russia’s status as a significant oil and commodities producer, particularly for Europe. This situation remains a wildcard, and could give way to more choppiness and even higher prices in the near term – an outcome we think would simply shift supply elsewhere, and bring even more producers online.

What are the implications of investors now that Russia has invaded Ukraine?

“From the start of WWII in 1939 until it ended in 1945, the Dow was up 50%, more than 7% per year,” noted institutional analyst Ben Carlson of Ritholtz Wealth Management. Between 1914 and 1945, a period that includes two of the worst wars in U.S. history (WWI and WWII), the Dow was up a combined 115%, according to Carlson and S&P Dow Jones Indices. In another study conducted by Ned Davis Research, they examined the 28 worst political or economic crises over six decades before the 9/11 attacks in 2001. In 19 cases, the Dow was higher six months after the crisis began. The average six-month gain following all 28 crises was 2.3%.

In the aftermath of 9/11, which left stock markets closed for several days, the Dow fell 17.5% at its low but recovered to trade above its September 10th level by October 26th, six weeks later. Should investors reduce exposure to stocks because of the fear of a war between Russia and Ukraine? History would suggest that exiting the stock market now would be the wrong decision.

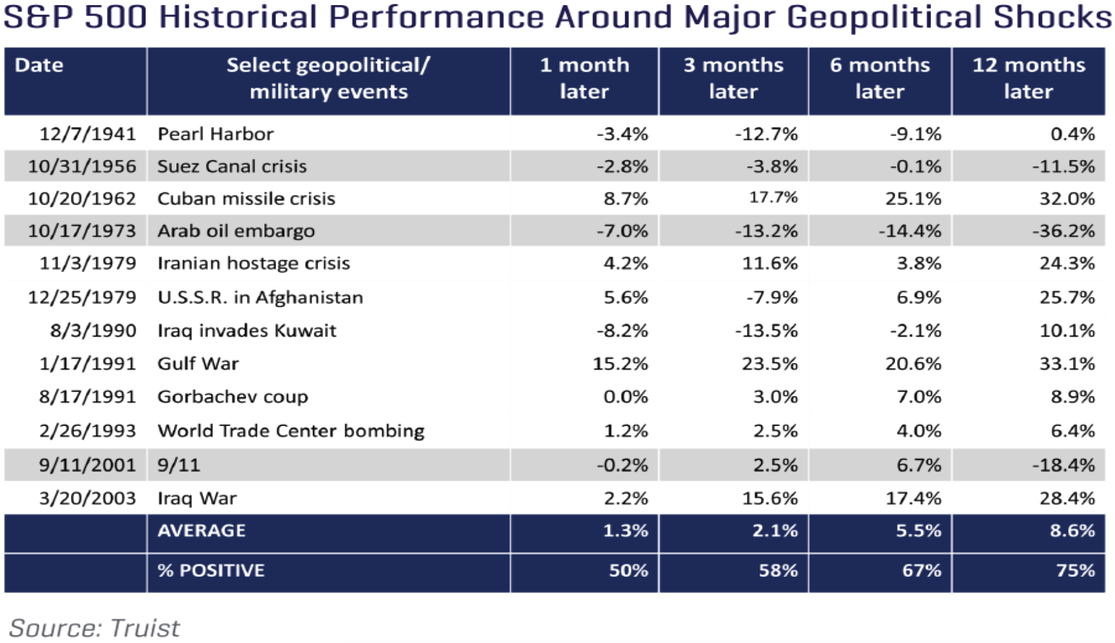

How have markets reacted in the past to major geopolitical events?

According to a study conducted by Truist co-chief investment officer Keith Lerner, “in nine of the last 12 geopolitical shock events, the S&P 500 Index was higher 12 months later, with an average 12-months return of 8.6%”

The Truist report notes that the three highlighted instances in the graph, where stocks were down a year later, coincided with a recession. However, the major finding of the study shows “that the history of these types of events tend to have a fleeting market impact unless they lead to a recession.” At this time, the consensus of almost all analysts indicates a very low to non-existent risk of a recession.

Bottom Line for Investors

The U.S. Stock Market & The U.S. Economy Are Separate Entities. Higher oil prices are not ideal for energy-intensive businesses or consumers, but they are also not a death knell for earnings or an economic expansion. The U.S. economy was notably weaker in the 2011 to 2014 period than it is today, in our view, and the economy and markets managed to do just fine during that period of $100+ oil.

It may not happen immediately but eventually sustained higher prices will encourage more production, particularly from U.S. shale companies. We are starting to see signs of that now. As production ramps up and more supply comes online, price pressures will eventually ease, in my view. I do not necessarily see this as a multi-year process as we saw in the previous cycle – U.S. shale companies can bring production online relatively quickly and efficiently, and with oil close to $100 per barrel, I believe they will.

Investors often sell first and ask questions later. The one thing investors need to remember is that Russia invading Ukraine will have almost no impact on the underlying U.S. economy. The U.S. doesn’t buy much of anything from Ukraine and, because of sanctions, we buy and sell very little to and from Russia. We import only about $1.1 billion a year from Ukraine. We import only about $24 billion a year from Russia out of $2.8 trillion in trade from the rest of the world. Depending on how long the war lasts, the invasion will have only a small, short-term impact on the U.S. stock market. Over time, it is unlikely this will change the outlook for corporate profits or U.S. economic fundamentals. Any decline in the stock market would be temporary and could present itself as a buying opportunity.

- Bloomberg. February 8, 2022. https://advisor.zacksim.com/e/376582/opinion-articles-20/44vsb7/442701246?h=cQ_MkO6nfPMtis8sR04iV83vg3rEe9eat-wLX7uh5wU 22-02-08/america-s-frackers-are-back-and-they-renow-a-threat-to-opec

- Fishers Investments. February 2, 2022. https:// www.fisherinvestments.com/enus/marketminder/our-perspective-on-those-100-oilforecasts

- Fred Economic Data. February 9, 2022. https:// fred.stlouisfed.org/series/DCOILWTICO

- Fred Economic Data. February 15, 2022. https:// fred.stlouisfed.org/series/SP500#0

DISCLOSURE: Past performance is no guarantee of future results. Inherent in any investment is the potential for loss.

Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.